Invest Smarter, Pay Less in Taxes, Keep More of Your Retirement Wealth.

We combine professional investment management with integrated tax planning — including daily tax-loss harvesting, direct indexing, and zero-cost trading — to help retirees keep more of what they’ve earned.

If you’d like to see how these strategies could improve your after-tax results, schedule a short conversation with our team.

Want to see what it is like to be a client of the firm? Every Friday we send our clients a market update about what we are watching in the markets, politics, and more.

You will receive the same emails as our current clients. Those emails do not contain ads or promotions, it is not marketing material but rather our real, weekly communications with paying clients.

Direct indexing gives retirees:

■ Market exposure similar to an index

■ Hundreds of harvestable tax lots

■ Control over gains during withdrawals

■ The ability to remove industries or concentrated positions

■ Better long-term tax efficiency

■ This is the modern way to invest in retirement.

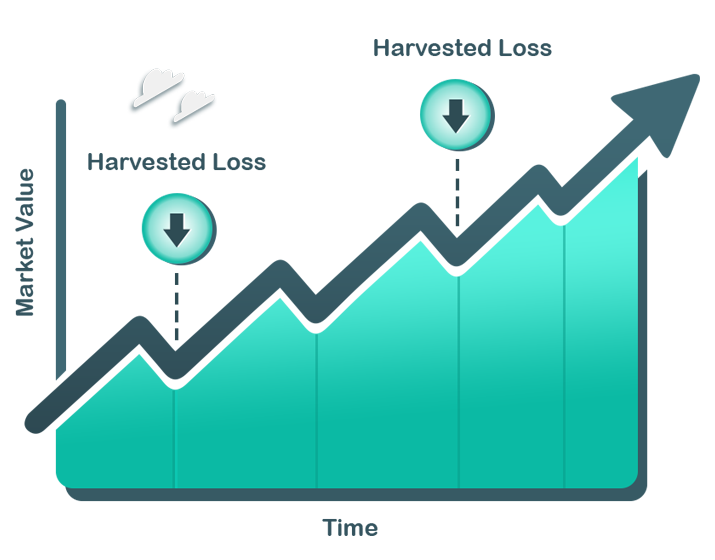

Daily harvesting means:

■ More captured losses

■ More tax savings

■ More money compounding in your portfolio

Our algorithmic tax-loss harvesting system evaluates your portfolio every trading day, looking for losses created by normal market movement. The goal is simple: capture tax-saving opportunities without changing your long-term investment exposure.

How the system identifies harvesting opportunities:

■ Scans every individual tax lot daily for unrealized losses

■ Looks for “micro-dips” caused by routine volatility

■ Confirms that realizing a loss will not push the portfolio too far from its target allocation

■ Prioritizes losses that can offset future gains and reduce your overall tax bill

Once a loss is harvested, the system immediately reinvests the proceeds so your market exposure stays intact.

How reinvestment and wash-sale avoidance work:

■ Buys a highly correlated replacement security to maintain similar market exposure

■ Avoids wash-sale violations by selecting approved substitutes

■ Continues monitoring the new position, evaluating when to transition back to the original holding

■ Uses tax-aware rebalancing to keep risk and allocation aligned with your plan

In this complimentary white paper, we explore common mistakes and misconceptions retirees make when estate planning.

Click the button below to download immediately, no email or contact information is required.

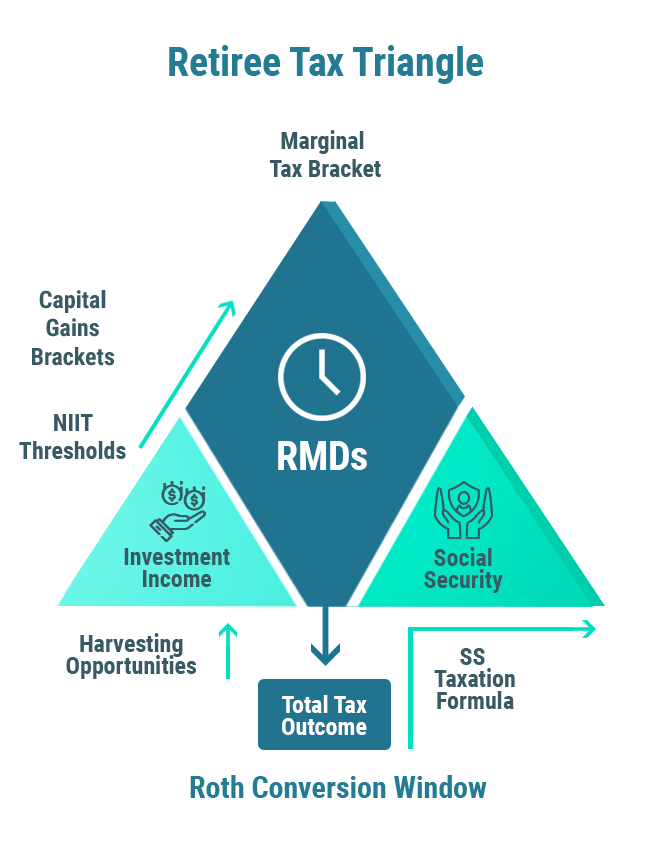

Retirees face a unique combination of tax challenges — and opportunities — that make tax-efficient investing far more impactful than during working years.

Our tax-integrated investment approach helps retirees reduce taxes by coordinating:

This is how retirees reduce taxes — not by guessing, but through deliberate planning that keeps more of their wealth working for them.

We review your current investments, tax return, income needs, and long-term goals.Your portfolio is designed for efficiency — and customized to your tax situation.

We monitor your accounts every trading day, capturing losses and reducing drift.Zero-cost trading allows us to harvest losses frequently and intelligently.

When you need income, we sell the most tax-efficient assets — not just the easiest ones.Withdrawals are coordinated with your RMDs, Social Security, and tax brackets.

We prepare your tax return and review it with you to identify opportunities for next year.Your investment and tax plan stay aligned every year.

Click below to schedule a complimentary meeting with us to hear about what we can do for you

Schedule A Complimentary Meeting

Sentinel Wealth, with your input, will develop an investment strategy that seeks to achieve your particular investment goals and objectives.

Our advisors will develop a strategic asset allocation that is targeted to meet you investment objectives, time horizon, financial situation and tolerance for risk.

We will develop a portfolio for you that is intended to meet the stated goals and objectives. We manage different portfolios and the construction may consist of blending allocations to two or more portfolios

We will provide investment management and ongoing oversight and rebalancing of your investment portfolio as needed.

We will provide monthly reports to your secure client portal that consists of performance data, and all activity in the accounts for the month. In person reviews are also conducted on a routine basis.

Many of our clients use a blend of these portfolios as determined by risk tolerance. New clients will complete a questionnaire that aids us in the customized construction of portfolios for each client’s individual needs.

The Core Equity Model seeks to grow assets through investment in individual stocks with very strong fundamentals and mostly large cap holdings.

This is a moderately aggressive portfolio.

Investor type is moderately aggressive. A moderately aggressive investor values reducing risks and enhancing returns but would like exposure to some of the more aggressive holdings and is willing to take on modest risks to do so.

A moderately aggressive investor may endure periods of loss of principal and lower degree of liquidity in exchange for long-term appreciation.

The Fixed Income Model seeks to grow assets through investment in fixed income holdings, preferred stocks, and bonds with strong dividends or other types of distributions to stakeholders

Investor type is conservative. A conservative investor values protecting principal over seeking appreciation. This investor is comfortable accepting lower returns for more liquidity and/or stability

Typically, a conservative investor primarily seeks to minimize risk and loss of principal.